You may be able to turn £800 into £5,500 in your state pension

Clare Casalis and Amalia Illgner | Edited by Ben Slater

There is a potentially unbeatable opportunity everyone aged 45 to 72(ish) needs to consider. You’ve got until 5 April 2025 to buy back any missing national insurance years from 2006 to 2016. This can be prove very lucrative, as some are on course to make over £50,000 in boosts to their state pension by following this guide.

– Under 45? Go through the exercise anyway. While it is more marginal to check if it’s worth topping up, you may find a partial year worth buying.

– Aged between 70 and 72(ish)+? This is for men born after 5 April 1951 (currently aged 72) and women born after 5 April 1953 (currently 70). Born earlier? You’re on the old state pension, so this doesn’t apply.

In this guide

- Why national insurance years are important

- Step 1: First watch Martin’s NI record video explainer

- Step 2: Check your state pension forecast

- Step 3: Can you plug NI gaps for free?

- Step 4: Should you pay to boost your state pension?

- Step 5: Is it worth it?

- Step 6: Contact the Future Pension Centre

- Step 7: More to bear in mind

- How to buy extra NI years

- FAQs

You now have extra time to boost your state pension by £1,000s

You now have until 5 April 2025 to pay voluntary national insurance (NI) contributions on gaps in your NI record between 2006 and 2016.

This is the second deadline extension – it was previously changed from 5 April to 31 July 2023 – and follows reports that Government helplines have been completely overwhelmed in recent months, preventing callers from being able to get the necessary advice.

In addition to extending the deadline, the cost of paying voluntary NI contributions will remain frozen until 5 April 2025.

So if you’re years away from state pension age, you’ve more time to decide if paying to plug gaps in your NI record is right for you – just don’t put it off too long. If you’re almost (or already) at state pension age, and doing this is right for you, you shouldn’t put it off at all to ensure you get the maximum benefit from paying to plug gaps in your record.

Why national insurance years matter

The full ‘new’ state pension is currently £203.85 a week – however how much you receive depends on how many ‘qualifying’ full national insurance (NI) years you have. Most collect NI years through working and paying NI, but you can also get them if you’re claiming benefits or caring for others.

In general, you need around 35 full NI years to get the maximum state pension, though some will need a lot more (we’ve seen examples of people needing 44+ years) depending on your age and NI record up to now.

There is a strict time limit on buying back years.

Normally you can buy back up to six years, but when the ‘new’ state pension was introduced, transitional arrangements were put in place to let you plug gaps all the way back to 2006.

This was due to end on 5 April 2023, and then 31 July 2023, but because so many people are trying, the necessary government phone lines are clogged up (mainly due to Martin shouting from the rooftops about it). So the date has been extended to 5 April 2025.

This is big money, as Martine emailed…

“After listening to Martin’s podcast, I checked my NI contributions and found I had eight years missing! I’ve now paid six years and will pay the next two years when possible. This has made a difference of about £49 a week which is considerable! I’d never have known without the podcast! Thank you.”

– MoneySaver Martine

To put that in context, Martine paid up to £5,000 (it may’ve been far less) to increase her state pension by £2,550 a year. If she lives for the typical 20 years after state pension age, that’d be a total uplift of around £51,000… and it’s inflation-proofed.

So, for some, paying to plug NI gaps is a no-brainer that could massively boost your pension. Yet there are lots of ‘ifs’ and ‘buts’ that could mean it’s not right for you, so let us take you through it step by step.

Step 1: First watch Martin’s NI record video explainer

Watch Martin explain how this works in more detail below before tackling the steps to see if it’s something you need do (or if radio’s more your thing, you can listen to him explain it on his BBC podcast).

https://youtube.com/watch?v=ZGXGKaNBVZg%3Fenablejsapi%3D1%26origin%3Dhttps%253A%252F%252Fwww.moneysavingexpert.com%26widgetid%3D1

This video is from ITV’s The Martin Lewis Money Show Live, which was broadcast on Tuesday 21 February 2023. Note: Martin refers to a deadline of 5 April 2023 in the video, but this was extended to 5 April 2025.

Step 2: Check whether you’re missing any NI years since 2006

The first two checks you need to do are simple:

CHECK 1: Check for unfilled years in your NI record…

Here you need to:

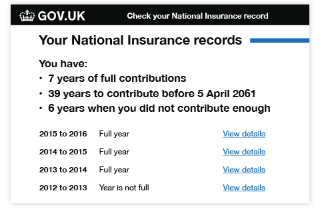

Check your national insurance record

This shows your full national insurance record. And for each year since you were 16, it will either say ‘Full year’ or ‘Year is not full’. The ‘View details’ link will give you more information.

If you have ‘non-full’ years since 2006, it could be worth paying to plug these to get a higher state pension. The rest of this guide deals with whether you should and how to do that.

CHECK 2: If you have missing years, then get your state pension forecast…

You need to use the Government’s:

State pension forecast calculator

This will give you two pieces of information:

– How much state pension you’d get based on your NI record to date.

– A forecast of how much state pension you’re likely to get if you work up to your state pension age.

If your forecast ISN’T for the full £203.85 a week, and you have gaps in your NI record, you may be able to boost years to get to the full amount.

There’s a link in your forecast to do this, or you can use the link in the box above. Once you’ve checked your NI record, go to step 3.

Warning. Don’t buy missing years if you’re due a full state pension.

For those projected to get, or already getting, a full pension… even if you’ve missing years, buying them won’t boost your pension, as you can’t get more than the full pension (and if you miss future years, you can always buy them then).

MSE weekly email

FREE weekly MoneySaving email

For all the latest deals, guides and loopholes simply sign up today – it’s spam-free!

FAQs Privacy Past Emails Unsubscribe

Step 3: If you have gaps in your record, see if you can plug ’em for FREE with NI credits

It’s not only work that earns you NI years. A range of scenarios see you build up NI entitlement automatically. (There are a few issues currently with adding NI years if you’re claiming universal credit.) Yet some credits need to be claimed manually to fill gaps – see if any of these scenarios fit:

– Caring for a child in the family: As long as you are/were between 16 and state pension age. If it is your child, only one parent can claim the credits via Child Benefit, but you can transfer the credit from one parent to the other – see our Child Benefit guide. If the family member is/was under 12 and not your child, see our Grandparents’ childcare credit guide for more info.

– Statutory sick pay: You are/were on it and not earning enough for a qualifying year.

– Unemployed and actively looking for work: You needn’t have been claiming jobseeker’s allowance, but will need to prove you were looking for employment.

– Employment and support allowance: Eligible for it, but not claiming it.

– Caring for a sick/disabled person: If it is/was for at least 20 hours a week. See our separate Carer’s Creditguide on this for more details.

–On jury service: You are/were on it and aren’t/weren’t self-employed.

– Wrongly imprisoned: As long as your conviction has since been quashed.

– A foster carer (kinship carer in Scotland): Since 6 April 2010.

– On statutory maternity, paternity or adoption pay: You are/were on it and didn’t/won’t earn enough for a qualifying NI year (additional statutory paternity pay also counts).

– Spouse of a member of the armed forces: You’re married to, or are a civil partner of, a member of the armed forces and went with them on an overseas posting (additional eligibility rules apply here).

– On a Government-approved training course: You are/were on one, are over 18, and weren’t sent on the course by Jobcentre Plus.

Full information on how to manually apply for any NI credits you’re due is on the Government’s national insurance credits page.

Most will have already got any NI credits they’re due. But if you haven’t, make sure you claim them and then start this process again.

Step 4: Work out if you should pay to boost your state pension

If a shortfall in state pension is likely and you’ve NI gaps in the years 2006 to 2016, you need to decide by the deadline of 5 April 2025 whether to top up. Some help…

- Those at or near state pension age will find it relatively easy to see if topping up may help. If your state pension is, or is forecast to be, less than £203.85 a week, and you won’t be able to plug gaps by any other means, topping up could be a no-brainer.

- For those older than 45 but still some way off state pension age it’s more of a toss-up, as you may still fill the gaps naturally. The younger you are, the more time you have to earn enough qualifying years before you reach state pension age.

- For most under the age of 45, it probably won’t make sense to pay for full NI years, but it might be worth checking if you can upgrade partial years on the cheap. If you’ve gaps in your NI record that you’re certain you won’t make up (for example, if you’ve moved overseas), or if you’re really worried about not being on track and want some extra peace of mind, it might be worth checking if you have any partial years in your record, as these can sometimes be upgraded to full years for as little as £15 – we’ve more details below.

It worked for Caroline, who emailed:

I am absolutely delighted… I was only one week short of a full year. I’ve paid a one-off payment of £15.40 [voluntary class 3 national insurance 2021/22 rate] to get an extra £127.92 per year on my state pension. So once again a success!

– MoneySaver Caroline

Important: If you were ‘contracted out’ of the additional state pension before 2016, topping up may not help.

Much here depends on your NI record from that period and it’s difficult to generalise. So it’s doubly important to call the Department for Work and Pensions’ helplines in step 6 to understand if paying to plug any NI record gaps will actually result in you being paid more state pension.

You’re more likely to have been contracted out if you worked in the public sector. You can check by looking at a pre-2016 payslip or P60 – if the NI contributions line has D, E, L, N or O next to it, you were contracted out.

Step 5: Use our calculator to see what topping up could be worth

Right now buying a full national insurance (NI) year costs £824, unless:

- You’re topping up the two most recent tax years, in which case it’s about £20 to £30 cheaper, as you pay the original rate for those tax years.

- You’re self-employed.

- You’re topping up a partial year, in which case it’ll cost less to make it a full year.

Use our calculator below to see how much buying NI years could be worth, then look at our life expectancy tables to work out if you’ll likely live long enough to benefit.

The maths is simple. A full NI year usually costs £824 and adds up to £302.64 each year to your pre-tax state pension. Get this maximum gain and it’s worth it as long as you live at least three years after getting your pension (or three years after you top up, if you’re already getting it).

Note that you can’t pay to increase your state pension beyond the maximum of £203.85 a week, so if you’re projected to get £200 a week or more, topping up is less good value for money.

Our calculator gives an indication of the maximum amount buying different numbers of NI years could be worth in today’s money.

Note: This tool is a ready reckoner – we’re working on an update to take into account the recent 10.1% increase to the state pension.

State pension top-up ready reckoner

How many years of voluntary NI contributions are you buying?1 year2 years3 years4 years5 years6 years7 years8 years9 years10 years11 years12 years13 years14 years15 years16 yearsCALCULATE

How long are you likely to live?

The potential gains to be made from buying voluntary NI contributions are huge. But one of the factors it depends on is if you’ll live long enough to gain. Consider your health and use our life expectancy tables below to see if you’re LIKELY to benefit.

Using data from the Office for National Statistics’ life expectancy calculator, the tables show how many more years people in different age groups can expect to live on average…

How long you’re likely to be getting the state pension

| Current age | Age at which you qualify for the state pension | Average life expectancy |

| 40 | 68 | 87 |

| 45 | 67 | 87 |

| 50 | 67 | 87 |

| 55 | 67 | 87 |

| 60 | 67 | 87 |

| 65 | 66 | 87 |

| 70 | You were eligible at 62 | 88 |

| 75 | You were eligible at 60 | 89 |

| 80 | You were eligible at 60 | 90 |

Life expectancy data provided by the Office for National Statistics.

Step 6: WARNING – don’t pay until you’ve called the Government’s pension helplines

We’ve given you a general idea of how this works. But there are many complexities, so the only way to know for sure if this is likely to benefit YOU is to get personalised information from the Future Pension Centre or the Pension Service.

Both services provide specific information about your current national insurance record. They’ll tell you whether doing so will actually result in any increase to your (eventual) state pension. It is possible to pay to plug a gap and see no gain, which is why this step is so important.

If you’re not yet at state pension age…

You need to:

Contact the Future Pension Centre on 0800 731 0175

It’s free to make the call (though you may be waiting a while, or need to try multiple times, as lines are currently very busy). The lines are open between 8am and 6pm, Monday to Friday. Full contact information is on the Future Pension Centre pages.

If you’re already at state pension age…

If you’ve deferred your state pension or are already claiming it, you need to:

Contact the Pension Service on 0800 731 0469

It’s free and phone lines are open between 8am and 6pm on Monday to Friday. See full Pension Service contact info.

Yet the Future Pension Centre in particular has been very busy and many have reported long waits or just not being able to get through. Martin’s tips…

Martin: ‘Struggling to get through to the Future Pension Centre?’

“The phone lines have been clogged due to unprecedented demand (some of the creation of which is laid at my door), as it’s a crucial part of the process. It’s a frustrating situation. Yet it’s also important to help reduce unnecessary demand on the Future Pension Centre, so only those who need to call do. Here are my three need-to-knows:

- Only call if a) you know you’ve gaps from 2006 onward and b) you’re not projected a full state pension.

– If you’re calling about pre-2006 years, you can’t buy them, don’t bother calling.

– Not sure of your gaps? Just check your national insurance record online.

– Not sure if you’re due a full state pension? Just check your forecast online. - The Future Pension Centre is only for those who haven’t reached state pension age.

If you’ve hit state pension age and want to buy years, call the Pension Service on 0800 731 0469. - The deadline to buy years has been extended until 5 April 2025, so there’s still plenty of time.

– There is no ‘good time’ to call sadly – no downtime – it’s luck at the moment if you get through.

– If you’re frustrated, give it a break, there’s still time and hopefully it’ll calm down.

MSE weekly email

FREE weekly MoneySaving email

For all the latest deals, guides and loopholes simply sign up today – it’s spam-free!

FAQs Privacy Past Emails Unsubscribe

Step 7: A few buts… not everyone will be better off if they buy more NI years

The Future Pension Centre or the Pension Service can tell you if paying for extra national insurance (NI) years will increase your state pension entitlement. But you need to think about the bigger picture (the Government helplines won’t help with that). Think about:

- If you’re likely to have a low income and will only rely on state pension, pension credit may cover the gap. Pension credit is a top-up for people of state pension age who don’t have a certain basic level of income. So there’s a risk you can get the same amount of cash with pension credit without paying to top up.

Though it’s worth us saying, there’s no guarantee that pension credit will still exist, be at the same level or have the same eligibility criteria when you retire. More info in Pension credit. - The gains from buying extra years may be reduced if it pushes you into a higher tax bracket. If you were to be near the threshold of either paying tax or hitting the 40% tax bracket once your state pension and other income is combined, you will pay (more) tax on your pension income if that income is higher.

This will mean it takes longer for you to breakeven on any voluntary NI contributions you make – though it’s likely to still be worth doing, even with this. Check out the latest tax rates and try our Income Tax Calculator to see if this might affect you.

How to buy missing NI years

If the Future Pension Centre or the Pension Service has said buying additional national insurance (NI) years would result in extra income and you’ve made the decision to top up, here’s how to do it:

- Decide how many NI years to buy. Do note that you don’t need to buy all the NI years you want in one go (though you will need to buy any between 2006 and 2017 before 5 April 2025).

- Contact HMRC to get an 18-digit reference number. To find the precise cost of the years you want to buy, and get the reference you need – this is important so they’re added to the right NI record and tax years. You’ll need to contact HM Revenue & Customs (HMRC). It can give you the number over the phone, or it takes 15 working days by post.

- Send the money to HMRC. Once you have the 18-digit reference number, send money through your bank or building society account to this HMRC bank account. Or pay by cheque, though HMRC says this takes longer to process.

- Wait for the extra NI years to be credited to your record. If you’re not yet claiming state pension, the payment can take up to 60 working days to process, after which you should see your NI record change.

If you are claiming state pension, HMRC will prompt the DWP to carry out a ‘benefit review’, so your payments won’t increase straightaway. However, the DWP will backdate the increase to the date you made the payment (NOT to the date you started claiming state pension).

FAQs

- How much do voluntary national insurance contributions cost?

- What if I’m self-employed?

- What if I’ve paid SOME national insurance, just not enough for a ‘full qualifying year’?

- I’m under 45, should I pay to plug gaps in my national insurance record?

- What if I live or work abroad?

- Is there a maximum number of missing years I can buy?

- Can I pay for voluntary national insurance contributions by monthly instalments?

- I claim universal credit, but my national insurance credits are not showing on my record

SOURCE: MSE (MARTIN LEWIS FOUNDER) WEBSITE